Germany is experiencing a battery storage boom, with total installed capacity reaching roughly 24 GWh after adding 6.57 GWh in 2025 alone an 8% year-on-year increase. For industrial decision-makers evaluating battery energy storage solutions, understanding the Germany Battery Energy Storage Market Outlook 2026 is critical. The market is accelerating due to renewable energy expansion, grid congestion, curtailment issues, and rising energy costs.

By end-2026, large-scale battery storage power is expected to double from 2.5 GW to 5 GW, with energy capacity more than doubling from 4 GWh to 9 GWh. Germany will likely deploy 2–3 GW of new BESS capacity in 2026, driven by solar and wind integration needs. This article provides the data-driven insights factory owners, plant heads, energy managers, and renewable developers need to make informed BESS investment decisions.

Germany’s Energy Transition and the Growing Need for Battery Storage

Germany is targeting 80% renewable electricity by 2030, with renewable generation capacity expected to reach roughly 300 GW against peak consumption of around 80 GW (IEA). This imbalance creates a constant need to balance supply and demand. BESS provides this balance by storing surplus energy and releasing it when needed, while also reacting fast to grid issues.

The rapid growth of renewables has fundamentally changed how volatility is managed in the energy system. Flexibility has become the new currency, and BESS is a crucial part of it. By balancing intermittent generation and supporting round-the-clock renewable supply, BESS is emerging as a cornerstone of the energy transition.

Germany continues to add renewable capacity at pace, creating a clear system-level need for storage to keep supply and demand in sync. Until the gap between renewable generation and flexible capacity closes, the need for batteries is absolutely real.

Current State of the Germany Battery Energy Storage Market

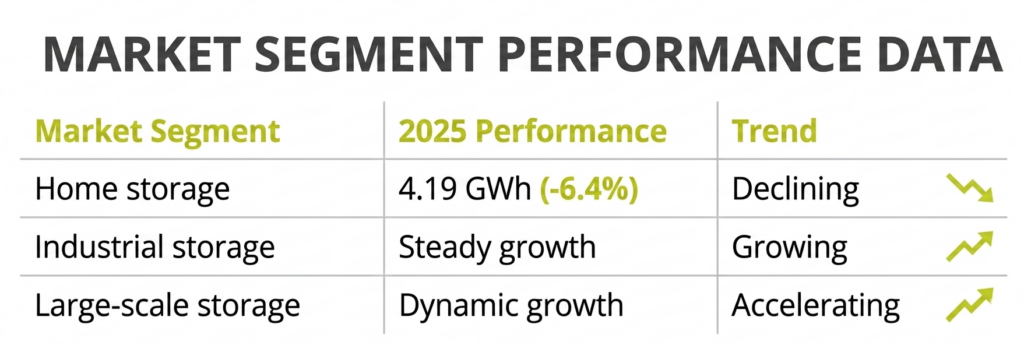

The Germany Battery Energy Storage Market Outlook 2026 shows strong momentum across multiple segments. In 2025, Germany added an estimated 6.57 GWh of stationary battery storage capacity, an 8% year-on-year increase. Total installed capacity now sits at roughly 24 GWh.

Around 530,000 new battery storage systems totaling about 5.84 GWh were commissioned and registered in 2025 (with late registrations expected to lift the final figure to 6.57 GWh). However, trends diverge sharply across segments:

Grid-scale BESS capacity reached roughly 2.4 GW by the end of 2025, with energy capacity around 3.5 GWh and an average system duration of about 1.5 hours continuing a steady multi-year climb in typical battery duration. By end-2026, longer-duration systems are expected to make up a growing share of new installations.

BVES, the German energy storage association, reported 31% revenue growth for German energy storage in 2025, with large-scale and plug-in (balcony storage) segments leading. The association’s own modeling projects large-scale battery storage power roughly doubling from 2.5 GW to 5 GW by end-2026, with capacity more than doubling from 4 GWh to 9 GWh.

Key Drivers Accelerating BESS Adoption in Germany

Renewable Energy Expansion

Germany’s renewable target 80% of electricity from renewables by 2030 necessitates scalable storage solutions to balance grid intermittency. The 2030 target of roughly 300 GW of renewable generation capacity against around 80 GW of peak consumption creates inherent volatility that BESS must manage.

Renewable curtailment is rising on both sides of the generation mix. In 2025, photovoltaic curtailment climbed sharply more than doubling year-on-year while combined onshore and offshore wind curtailment remained the larger absolute volume of the two. Germany curtailed a record amount of solar and wind power in the first half of 2025, with grid constraints and limited storage capacity preventing full use of available generation; roughly 8% of solar generation was curtailed in that period, more than double the share a year earlier.

Grid Congestion and Curtailment

In 2024 alone, network operators received 9,710 connection requests for battery storage at or above medium-voltage level, corresponding to around 400 GW of power capacity and roughly 661 GWh of energy capacity. Grid connection queues have become the central chokepoint for BESS deployment in Germany by some broader industry counts covering all storage projects above 1 MW, total requested capacity across Germany’s transmission operators has climbed well past 500 GW.

A lack of grid capacity is a critical bottleneck, driving higher levels of congestion and slowing the deployment of new generation, storage, and demand. Against this backdrop, German large-scale battery storage power is expected to double from 2.5 GW to 5 GW by end-2026.

Industrial Energy Cost Volatility

Electricity costs remain a major pressure point for German industry, though the relevant figure depends heavily on customer class. For electricity-intensive companies eligible for reduced network charges, the average price stood at roughly 10 cents per kilowatt-hour in late 2025. Industrial consumers without those exemptions continue to pay materially more. Germany’s day-ahead market spreads have widened substantially over the past several years as solar penetration has grown, creating real opportunities for flexible, dispatchable assets like batteries.

To address industrial competitiveness concerns, Germany introduced a subsidized industrial electricity price from January 2026: eligible energy-intensive companies receive compensation equal to 50% of the average wholesale price (with a 5 cents/kWh floor) on up to half of their annual consumption, running through 2028 under an EU state aid framework. The subsidy is conditional recipients must reinvest at least half of the aid into renewables, battery storage, or energy efficiency projects, directly linking industrial relief to storage adoption.

Energy Security and Reliability

Flexibility has become the new currency in Germany’s energy system. Batteries can offer strong returns when sized and operated correctly, balancing intermittent generation to support continuous renewable supply. The real issue is the persistent gap between renewable generation and flexible capacity.

High market volatility sends a clear signal: Germany needs more flexible assets, and batteries are a key part of the solution. BESS is vital for integrating renewable energy and keeping supply and demand in sync.

Major Battery Storage Applications in Germany

Commercial and Industrial Facilities

The fast-growing commercial and industrial BESS market is highly fragmented, spanning backup power, electric vehicle charging paired with storage, peak load management, and solar PV integration. From 2025, C&I users can apply Germany’s accelerated depreciation policy, with first-year depreciation rising from 30% to 50% for qualifying storage investments.

Solar + Storage Projects

Solar-plus-storage projects capture surplus generation during midday peaks and discharge during evening demand. With photovoltaic curtailment rising sharply through 2025, these projects directly address growing renewable waste. BVES reports the plug-in storage segment as one of the leading contributors to 2025 revenue growth.

Wind Energy Integration

Wind-paired BESS helps manage curtailment of onshore and offshore wind, which together represented the larger share of Germany’s 2025 curtailment volume. Co-location of storage with wind assets remains limited today and is concentrated mostly at existing fossil-fuel generation sites with available grid connections.

Grid Services

BESS in Germany primarily generates revenue through grid system services and arbitrage across day-ahead and intraday electricity markets. Ancillary services markets are comparatively small relative to the scale of incoming battery capacity and could become oversaturated in the medium term, which may compress that portion of project revenue over time. Day-ahead spreads have widened materially over the past several years, keeping arbitrage opportunities strong for now.

Challenges Facing the Germany Battery Energy Storage Market

Grid connection queues are the primary chokepoint. With roughly 400 GW of formally registered medium-voltage-and-above storage capacity requesting connection in 2024 alone and broader industry estimates across all storage projects running considerably higher connection pace, not battery availability, will decide how much of the pipeline actually gets built.

Policy design uncertainties could reshape project economics. Capacity market signals, ancillary services procurement reform, and grid fee regimes will all shape future revenue stacks and investor confidence.

Revenue volatility presents real risk. In other mature markets such as the UK, BESS revenues have in some cases fallen sharply within a single year as more storage capacity entered the market. Similar dynamics could emerge in Germany over time, particularly in the ancillary services segment, as more battery capacity competes for a comparatively fixed pool of grid-service revenue.

Market entry barriers remain for independent developers. Utilities still dominate larger-scale projects, often leveraging legacy grid connections that newer entrants don’t have access to. Whether independents can scale meaningfully beyond utility incumbents remains an open question.

Technology risk is increasingly manageable through equipment guarantees, standardized construction practices, and insurance products built specifically for storage assets. Market risk fluctuating prices, thinner liquidity, and shifting revenue sources remains the larger challenge for project economics.

Government Policies and Market Support Mechanisms

Germany has set a long-term goal of carbon neutrality by 2045, with intermediate targets driving continued policy support for storage.

Long-duration energy storage subsidies are planned to increase, alongside efforts to simplify grid connection processes and lower market access thresholds for new projects.

From 2025, C&I users installing energy storage can apply “accelerated depreciation,” with the first-year depreciation rate rising from 30% to 50%.

From January 2026, Germany’s new industrial electricity price scheme gives eligible energy-intensive companies compensation equal to 50% of the average wholesale price (subject to a 5 cents/kWh floor) on up to half their annual consumption, running through 2028 with recipients required to reinvest a portion of that relief into renewables, storage, or efficiency upgrades.

Grid operators received 9,710 connection requests in 2024 corresponding to roughly 400 GW of registered capacity at medium-voltage level and above, underscoring a massive project pipeline despite ongoing connection bottlenecks.

Market Forecast: Germany Battery Energy Storage Market Outlook 2026 and Beyond

The Germany Battery Energy Storage Market Outlook 2026 points to 2–3 GW of new BESS capacity deployment in 2026. Large-scale battery storage power is expected to double from 2.5 GW to 5 GW by end-2026, with capacity more than doubling from 4 GWh to 9 GWh.

Average battery system duration has been climbing steadily for several years and is expected to continue rising through 2026, reflecting deeper solar penetration and wider day-ahead price spreads that reward longer-duration assets.

Germany enters 2026 as one of Europe’s most attractive and complex markets for BESS, with deep electricity markets, volatile intraday pricing, and ambitious renewable targets. BESS is no longer peripheral to the energy transition it is becoming central to it.

Longer-term projections point to continued BESS capacity growth through 2030, supported by falling installation costs, rising electricity rates, and ongoing government incentives.

How Global Manufacturers Can Support Germany’s Storage Growth

India is emerging as a global manufacturing hub for Battery Energy Storage Systems, with growing capacity presenting real opportunities to export to Europe. GoodEnough Energy is part of that buildout, operating a 7 GWh annual manufacturing facility and offering a product range built specifically to span the market from the StorEDGE 0.25, a 250 kWh modular cabinet solution suited to commercial and industrial sites, up to the StorEDGE 5.0, a 5 MWh containerized system engineered for utility-scale deployment.

Achieving reliable round-the-clock renewable energy requires storage that holds up under sustained cycling, which is why every StorEDGE system uses liquid cooling thermal management rather than passive or air-cooled alternatives keeping cell temperatures stable through high-frequency charge-discharge cycles and supporting system lifespan under demanding duty profiles. Power conversion systems are built to European compliance certification standards, and the energy management system is developed in-house, giving GoodEnough Energy direct control over integration, dispatch logic, and the technical support it can offer EPCs and developers evaluating the platform.

Indian manufacturers more broadly offer competitive capabilities, supply chain advantages, and growing export readiness for European storage demand. GoodEnough Energy can support Germany’s projected 2–3 GW of new annual BESS deployment by leveraging its manufacturing scale to provide cost-competitive solutions with robust supply chains, as large-scale storage power in the German market is forecast to double from 2.5 GW to 5 GW by end-2026.

Global manufacturers support this shift by offering customized commercial and industrial configurations, including local installation, commissioning, and interfaces adapted to regional grid requirements backed by vertically integrated value chains that combine hardware, software, and service under one accountable supplier.

Conclusion

The Germany Battery Energy Storage Market Outlook 2026 reveals a market in rapid transformation, with roughly 24 GWh of total installed capacity and 2–3 GW of new deployment expected this year. Renewable expansion, grid congestion, curtailment, and industrial cost volatility are all accelerating BESS adoption.

Industrial decision-makers must evaluate revenue models, manage market risk, verify grid connection timelines, and leverage policy benefits like accelerated depreciation. The market is also moving toward longer-duration systems as solar penetration deepens and price spreads widen.

India’s emerging BESS manufacturing base including facilities like GoodEnough Energy’s 7 GWh production facility offers increasingly competitive solutions for European demand. Manufacturers like GoodEnough Energy can support Germany’s storage growth through scalable, cost-competitive systems built for the conditions this market actually presents.

The energy transition needs storage and partners who understand it both technically and strategically.